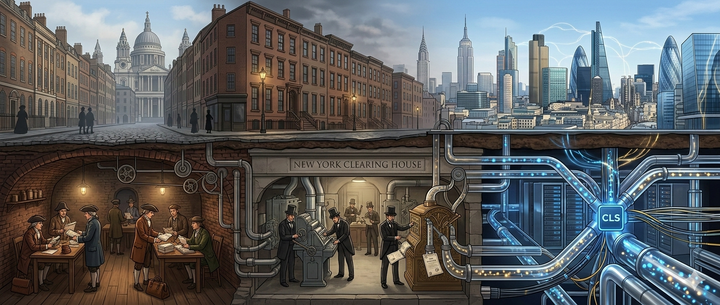

The four-layer framework: a complete liquidity risk assessment for DeFi

The complete DDD Episode 9 four-layer liquidity framework: pool depth, backstops, pipes, and hubs. From Jackson's Bank War to Rothschild's London nexus, 200 years of financial plumbing failures reveal what actually makes a DeFi position liquid under stress.

What 200 years of financial plumbing failures teach about evaluating any position in decentralized finance

The Druid Deep Dive Episode 9 started with a question that sounds simple: what makes an asset liquid? The answer, assembled across four parts spanning nearly two centuries of financial history, turns out to be far more layered than most DeFi participants realize.

The conventional approach to liquidity analysis in decentralized finance stops at pool depth. That is one-quarter of the picture. The four-part mini-series built a complete framework by peeling back one historical episode at a time, each revealing a layer of infrastructure that most market participants never think about until it fails. The framework applies to any DeFi position, any protocol, any chain. It is the product of studying what actually broke during crises, and what survived.

Here is the complete architecture.

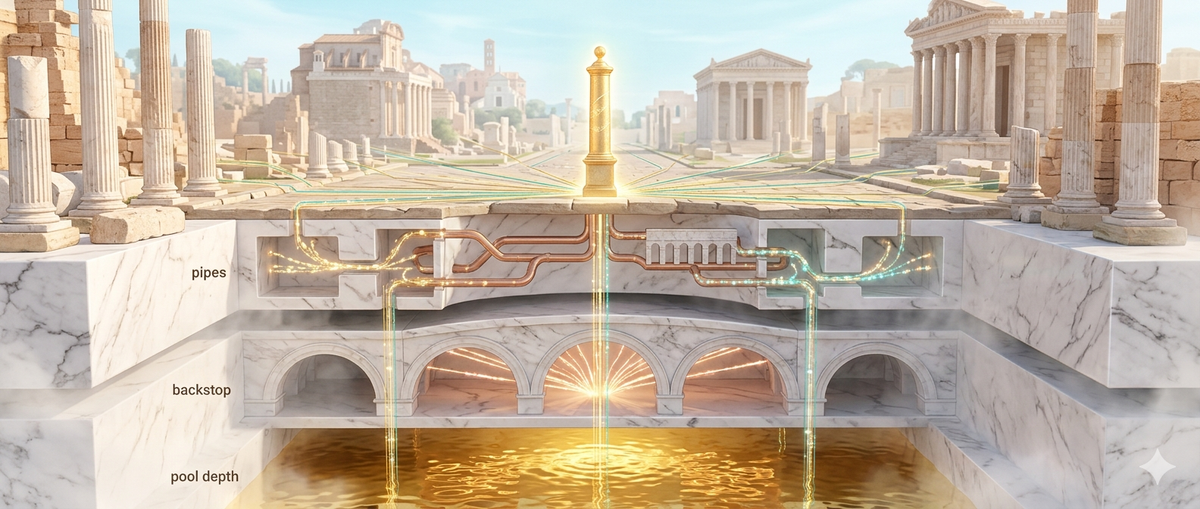

Layer 1: pool depth

Episode 9, Part 1: The bank war: Central vs. decentralized money examined the destruction of America's Second Bank and the Panic of 1837 that followed. The Second Bank of the United States held between 30% and 40% of the nation's gold and silver reserves and operated twenty-five branches forming the country's only interregional clearing network [1]. When Andrew Jackson destroyed it, he didn't just remove a central authority. He destroyed the deepest liquidity pool in the American financial system.

The consequence was instructive. When banks across the country suspended specie payments on May 10, 1837, even holders of physical gold found themselves trapped [2]. The asset was "safe." The infrastructure for exchanging it had evaporated. Farmers with gold in their pockets could not buy supplies because merchants had no way to make change, verify coin purity, or extend credit against it. The depression lasted nearly seven years [2], not because safe assets didn't exist, but because the markets for those assets had collapsed.

The DeFi parallel is direct. A governance token with strong fundamentals but $200,000 in DEX liquidity is the crypto equivalent of an Illinois farmer's gold in 1838: theoretically valuable, practically immovable under stress. Layer 1 asks: is there enough market depth to absorb your exit? Are there multiple venues, or does all liquidity concentrate on a single DEX?

Layer 2: the backstop

The Druid Deep Dive, Episode 9, Part 2: The Eurodollar shadow: when dollars escape their makerstraced the rise of a $13 trillion offshore dollar system that functioned beautifully for decades, until 2008 revealed it had no lender of last resort [3]. The Eurodollar market created dollar-denominated credit on a massive scale with no central bank backstop. When Lehman Brothers collapsed and European banks could not roll over their short-term dollar liabilities, the interbank lending market froze. The Federal Reserve had to lend nearly $600 billion through emergency swap lines to foreign central banks, effectively improvising a backstop for a monetary system it never created and could not directly control [4].

The swap lines worked. They narrowed the LIBOR-OIS spread by approximately two percentage points within weeks [5]. But the episode exposed a structural vulnerability that maps precisely onto stablecoin markets today: Tether, with a market cap exceeding $162 billion, functions as what analysts call a retail Eurodollar for the digital age [6]. It operates outside the US banking system, serves populations that cannot easily access domestic dollar infrastructure, and grows fastest precisely because it solves real problems. But when the Eurodollar market seized, the Fed stepped in because the offshore dollar system had become too interconnected with the onshore economy to allow it to fail. If a major stablecoin faces a confidence crisis, there is no equivalent swap line. No central bank has committed to backstopping digital dollar substitutes operating on public blockchains.

Layer 2 asks: is there a lender of last resort when confidence breaks? The Eurodollar system had the Fed swap lines. What does your stablecoin have?

Layer 3: the pipes

The Druid Deep Dive, Episode 9, Part 3: ¨The invisible pipes: how clearing systems made money move¨ went beneath both pool depth and backstops to examine the settlement infrastructure that doesn't create money, doesn't store money, but makes money move. Before 1853, New York banks settled accounts by sending porters to walk from bank to bank exchanging checks for bags of gold coin [7]. The New York Clearing House changed that, clearing $22.6 million on its first day of operation [7]. Today, it processes nearly $2 trillion daily and has maintained operations without interruption through every financial crisis since 1853 [8].

The most consequential lesson came from Bankhaus Herstatt's collapse in 1974. German regulators shut the bank down in the middle of the business day, after Herstatt's American counterparties had already paid out Deutsche Marks but before they received the corresponding dollars [9]. Over the three days following the failure, gross funds transferred through the interbank system declined by approximately 60% [9], not because money had been destroyed, but because banks stopped trusting the pipes. It took twenty-eight years to build the solution: CLS Bank, which settles over $6.5 trillion in foreign exchange instructions daily using payment-versus-payment mechanics that ensure both legs of a trade settle simultaneously or neither does [10].

DeFi's bridge exploits, including Ronin ($625 million), Wormhole ($320 million), and Nomad ($190 million), are settlement failures, not liquidity failures [11]. The pools existed on both sides. The pipes between them broke. The New York Clearing House operated through ten panics without interruption. Can your bridge say the same?

Layer 3 asks: can you move the asset to where depth exists? Are bridges and settlement channels operational, audited, and battle-tested?

Layer 4: the hub

The Druid Deep Dive, Episode 9, Part 4, "The hub: how Rothschild made London the nexus of everything," added the final layer. Nathan Rothschild's London operation became the dominant node in 19th-century global finance because it connected four markets that had previously operated in relative isolation: gold bullion, sovereign bonds, currency exchange, and merchant banking credit [12]. A merchant who needed to convert gold into a Prussian bond position didn't need to separately engage a bullion broker, a bond underwriter, and a currency dealer. He went to Rothschild. The hub absorbed the complexity.

From 1919 until 2004, the London Gold Fixing, the daily benchmark price for global gold, was conducted at Rothschild's New Court offices [13]. By the 1840s, the family had all but monopolized the markets for French and Belgian government bonds [14]. Their multinational structure meant they could issue a bond in one market and arbitrage price differences across all five Rothschild houses simultaneously, a capability no single-city bank could match.

The critical insight: gold was valuable in the 19th century partly because of its intrinsic properties, but mostly because Rothschild made it instantly convertible into bonds, currency, and credit through a single interface. An asset that cannot be efficiently converted into other asset classes through a trusted hub is, in a crisis, only as liquid as its single deepest pool.

DeFi today looks like pre-Rothschild European finance. A trader wanting exposure across stablecoins, liquid staking tokens, governance tokens, and real-world assets must navigate dozens of DEXs across multiple chains with different pool structures, fee models, and liquidity depths. DEX aggregators like 1inch and CowSwap are the early proto-hubs, but they operate primarily within single chains. Cross-chain aggregation remains fragmented.

Layer 4 asks: is there a nexus node that connects your asset's market to other markets efficiently? Can you convert between asset classes, from yield-bearing stablecoins to governance tokens to liquid staking derivatives, without navigating five separate settlement environments?

What most participants miss

Most DeFi participants evaluate only Layer 1. They check pool depth on a DEX, see reasonable numbers, and stop there. Sophisticated participants consider Layers 2 and 3, asking about backstops and bridge security. The Rothschild lesson adds Layer 4: the assets that retain value in a crisis are those connected to a hub that provides efficient conversion across multiple markets.

The complete framework is cumulative. A position with deep pools (Layer 1) but no backstop (Layer 2) is the Eurodollar system before 2008, functional until it isn't. A position with both depth and a backstop but broken pipes (Layer 3) is gold in an Illinois farmer's pocket during the Panic of 1837, safe but immovable. A position that clears the first three layers but lacks hub connectivity (Layer 4) is a well-collateralized asset stranded on a single chain with no efficient path to other markets, liquid in theory and isolated in practice.

The four-layer assessment is not a guarantee. It is a diagnostic. It forces the question that matters most during a crisis: not "is my asset valuable?" but "can I actually use it?"

Watch the series

The complete Episode 9 series is also available as narrated videos:

Part 1: The bank war: central vs. decentralized money

Part 2: The Eurodollar shadow: when dollars escape their makers

Part 3: The invisible pipes: how clearing systems made money move

Part 4: The hub: how Rothschild made London the nexus of everything

Sources and references

[1] Remini, Robert V. Andrew Jackson and the Bank War. W.W. Norton, 1967. As cited in DDD Episode 9, Part 1.

[2] Rousseau, Peter L. "Jacksonian Monetary Policy, Specie Flows, and the Panic of 1837." Journal of Economic History 62, no. 2 (2002): 457-488.

[3] BIS Committee on the Global Financial System. "US Dollar Funding: An International Perspective." CGFS Papers No. 65. Bank for International Settlements, June 2020.

[4] Fleming, Michael J. & Klagge, Nicholas J. "The Federal Reserve's Foreign Exchange Swap Lines." Federal Reserve Bank of New York, Current Issues in Economics and Finance 16, no. 4 (2010).

[5] Goldberg, Linda S., Kennedy, Craig & Miu, Jason. "Central Bank Dollar Swap Lines and Overseas Dollar Funding Costs." Federal Reserve Bank of New York Economic Policy Review 17, no. 1 (2011): 3-20.

[6] Catalini, Christian & de Gortari, Alonso. "On the Economic Design of Stablecoins." Working Paper, 2024. Available at SSRN.

[7] The Clearing House. "History." Official institutional history. Available: https://www.theclearinghouse.org/about/history

[8] The Clearing House. "About Us: Key Facts." Available: https://www.theclearinghouse.org/about

[9] BIS Committee on Payment and Settlement Systems. "A Glossary of Terms Used in Payments and Settlement Systems." Bank for International Settlements, March 2003.

[10] CLS Group. "What We Do." Available: https://www.cls-group.com/about/what-we-do/

[11] Chainalysis. "Cross-Chain Bridge Hacks." The 2023 Crypto Crime Report. Chainalysis Inc., 2023.

[12] Ferguson, Niall. The House of Rothschild: Money's Prophets, 1798-1848. Viking, 1998.

[13] London Bullion Market Association. "A Brief History of the Gold Fix." Available: https://www.lbma.org.uk

[14] Gille, Bertrand. Histoire de la Maison Rothschild, des origines à 1848. Librairie Droz, 1965.

[15] Atlantic Council. "Central Bank Digital Currency Tracker." GeoEconomics Center, 2025. Available: https://www.atlanticcouncil.org/cbdctracker/

[16] Shin, Hyun Song. "Big Techs in Finance: A New Paradigm?" Bank for International Settlements, Annual Economic Report, Chapter 3 (2019).

Legal disclaimers and disclosures

Educational purpose only: This content is provided exclusively for educational and historical research purposes. It should not be construed as investment advice, financial planning guidance, policy recommendations, or official economic analysis. Any contemporary parallels or policy discussions are presented as academic analysis, not recommendations for action. Historical patterns provide context for learning but do not predict future financial system outcomes or investment performance.

AI-assisted research disclosure: This historical analysis was researched and written with substantial assistance from artificial intelligence technology (Claude, Anthropic). While extensive efforts were made to verify all statistical claims, citations, and institutional analysis against authoritative sources, readers should independently verify any information before relying on it for academic, professional, investment, or policy purposes.

Accuracy and liability limitations: While extensive effort has been made to ensure historical accuracy through authoritative sources, the authors make no warranties about completeness, accuracy, or currency of information. Historical interpretation involves scholarly judgment and academic debate. Economic data may contain revisions, measurement inconsistencies, or reporting variations across different time periods and institutional sources.

Liability protections: The authors, publishers, and Sagix Apothecary assume no responsibility for errors, omissions, or consequences arising from the use of this information. This includes any errors that may result from AI assistance in research, writing, or data analysis. Users assume full responsibility for any decisions or actions taken based on this content.

Investment risk warning: Historical financial analysis does not constitute investment advice or recommendations. Past performance, whether historical or hypothetical, does not guarantee future results. All investments carry risk of loss, and readers should conduct their own research and consult qualified financial advisors before making investment decisions.

No professional relationship: This content does not create any professional, advisory, fiduciary, or client relationship between the reader and Sagix Apothecary, its authors, or affiliated entities. Readers seeking financial, investment, legal, regulatory, or policy guidance should consult qualified professionals licensed in their jurisdiction.

Methodological note: This analysis synthesizes findings from multiple Federal Reserve Bank research departments, National Bureau of Economic Research publications, peer-reviewed academic journals, and authoritative government historical records. The numbered citation system allows readers to verify specific claims against original sources rather than relying on secondary interpretations. All quantitative data and statistical analyses are drawn from the referenced academic literature rather than independent calculation.

Contemporary financial systems: References to modern financial systems, cryptocurrency protocols, or DeFi mechanisms are made for educational comparison purposes only. These comparisons do not constitute endorsements, recommendations, or predictions about the performance or suitability of any current financial products or services.

Publication information: Last Updated: March 2026 | Series: The Druid Deep Dive | Publisher: Sagix Apothecary

Publisher: The Genesis Address LLC