The Druid Deep Dive, Episode 9, Part 4: The hub: how Rothschild made London the nexus of everything

Explore the Rothschilds' 19th-century London hub: a nexus connecting gold, bonds, commodities, and FX markets, simplifying global settlements. Parallels to DeFi's need for aggregators, cross-chain tools, and oracles to unify fragmented liquidity and reduce complexity.

Historical period: 1811–1919

This is the forth part of our 4 episode series about liquidity and the backend internals of markets throughout history. Part 3 is here:

The missing layer: the nexus node

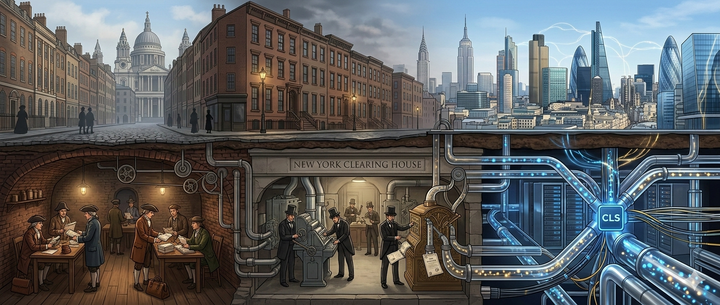

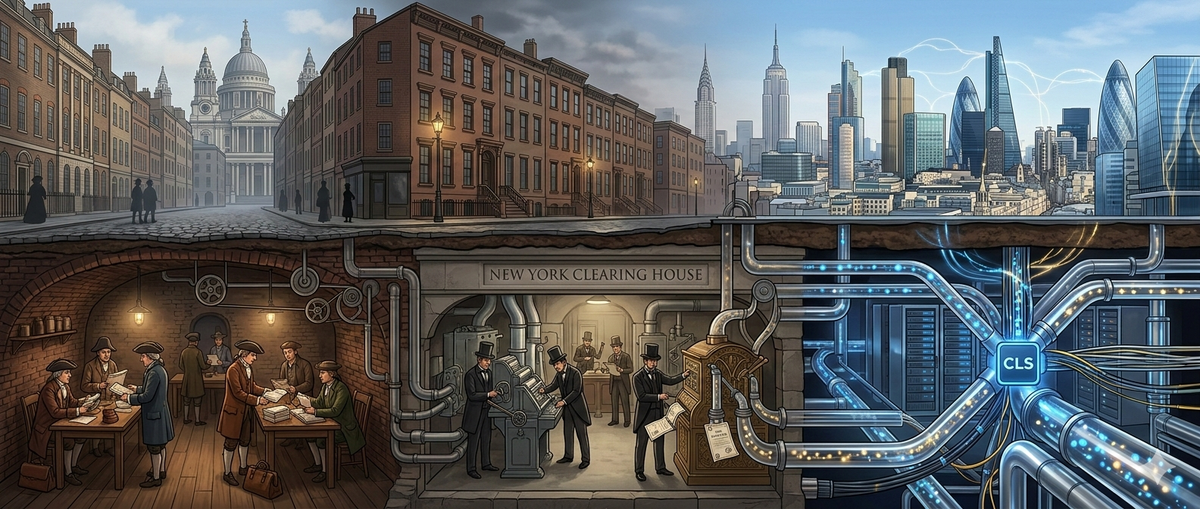

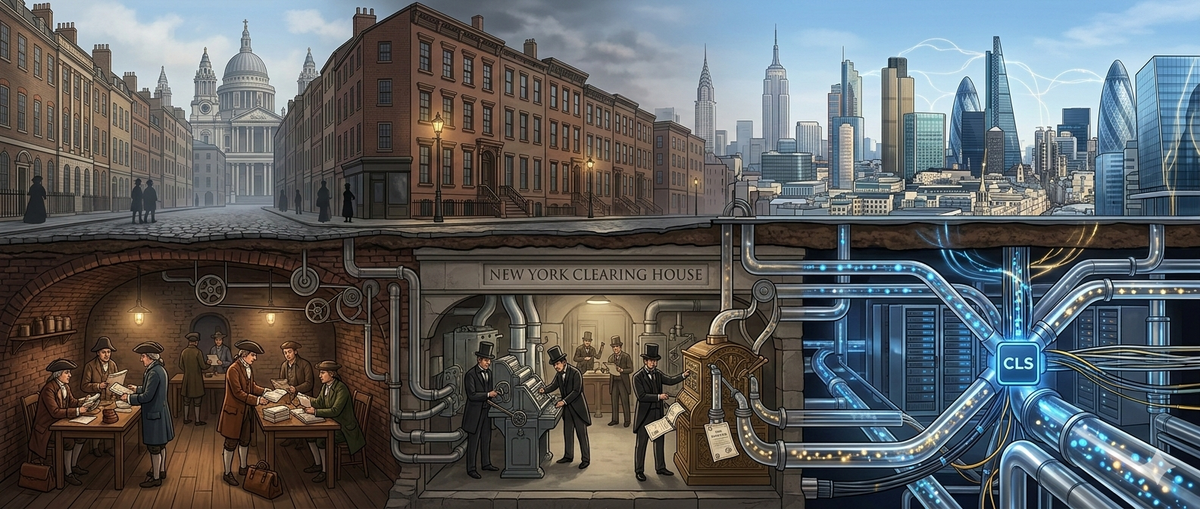

This mini-series has built a framework in three layers. Part 1 argued that the safe haven is the pool, not the token. Part 2 showed that pools need backstops — the Eurodollar system's $13 trillion in offshore dollars functioned beautifully until 2008 revealed there was no lender of last resort. Part 3 demonstrated that the pipes connecting pools are invisible infrastructure whose failure freezes everything — Herstatt risk, clearing house mechanics, and the boring plumbing that makes money move. Now we arrive at the fourth and final layer — the hub — the nexus node where multiple markets converge through a single trusted intermediary, so that traders don't need direct connections between every market. They clear through the hub.

The closest historical analogue is the London money market centered on N M Rothschild & Sons in the 19th century. The Rothschild network didn't create gold. It didn't create sovereign bonds. It didn't create foreign exchange. It sat at the intersection of all four — gold, bonds, commodities, and currency — and made them flow through a single point of convergence that reduced the entire world's settlement complexity.

How a Frankfurt coin dealer became the world's hub

The five-node architecture

Mayer Amschel Rothschild's strategic innovation was not financial engineering — it was network topology. By the 1810s, he had dispatched his five sons to the major financial centers of Europe: Amschel to Frankfurt, Nathan to London, Salomon to Vienna, Karl to Naples, and James to Paris [1]. Each brother ran an independent banking house, but they operated as a coordinated multinational unit, sharing information and dividing opportunities across borders [2]. Their coat of arms featured five interconnected arrows — an explicit symbol of unified nodes.

This structure was genuinely new. Previous court factors had concentrated their operations in a single city and served a single monarch. The Rothschilds created the first distributed financial network with coordinated settlement across multiple jurisdictions [2]. A government bond issued in Vienna could be simultaneously listed in London, Paris, and Frankfurt — a practice Nathan pioneered with the 1818 Prussian loan, where interest was payable in the market of issue rather than requiring investors to collect from a single location [3].

Nathan and London: the hub that won

While all five houses prospered, it was Nathan's London operation that became the dominant node. London's advantages were structural: it sat at the center of global shipping routes, it operated under English commercial law that was more favorable to creditors than Continental systems, and after 1815, Britain ran the world's largest trade surplus, meaning physical sterling and gold accumulated in London naturally [3].

Nathan exploited these advantages ruthlessly. From 1809 onward, he built a commanding position as a bullion broker in the City of London [4]. During the Napoleonic Wars, the British government engaged him to secretly obtain large quantities of gold to finance Wellington's armies — a task that required Nathan's network of couriers, dealers, and brokers across the Continent to move specie without alerting the French [4]. By 1815, the Rothschilds were not merely a bank. They were the operational layer through which international military finance flowed.

Why Rothschild became the hub

The convergence of four markets

Nathan's London house became the nexus because it connected four markets that had previously operated in relative isolation:

Gold bullion. Nathan established the family as the dominant bullion broker in London. In 1825, during a potentially catastrophic liquidity crisis, the Rothschilds supplied enough gold to the Bank of England to shore up its reserves and avert a panic [4]. In 1830, the Spanish monarchy handed the Rothschilds the rights to the Almadén mercury mines — and since mercury was essential for gold refining, this gave the family virtual control over the refining process [4]. When they acquired the lease on the Royal Mint Refinery in 1852, Rothschild became the institution through which the world's gold physically flowed [5]. From 1919 until 2004, the London Gold Fixing — the daily benchmark price for global gold — was conducted at Rothschild's New Court offices [6].

Sovereign bonds. The Rothschilds became the dominant underwriters and market-makers for European government debt. By the 1840s, they had all but monopolized the markets for French and Belgian government bonds [3]. They financed Brazilian independence (£2 million in 1825), Austrian military campaigns, Prussian reconstruction, and British imperial expansion [7]. Their multinational structure meant they could issue a bond in one market and arbitrage price differences across all five simultaneously — a capability no single-city bank could match.

Currency exchange. With houses in five currency zones, the Rothschilds were natural foreign exchange intermediaries. Transferring value from francs to sterling to florins to ducats was not a series of bilateral transactions — it was routed through the Rothschild network, which netted positions internally before settling only the residual balances with external counterparties. This is functionally identical to multilateral netting in a modern clearinghouse.

Merchant banking credit. Beyond bullion and bonds, the Rothschilds discounted commercial bills, provided trade finance, and extended credit to an elite clientele selected for political influence [3]. This meant that the same hub processing gold flows was also processing the commercial credit that financed international trade.

The network effect

The critical insight is that no trader needed direct relationships with every market. A merchant who needed to convert gold into a Prussian bond position didn't need to separately engage a bullion broker, a bond underwriter, and a currency dealer. He went to Rothschild. The hub absorbed the complexity. This is the same principle that makes DEX aggregators valuable: rather than routing manually across fragmented pools, the aggregator finds the optimal path through a single interface.

The Rothschild hub also generated an information advantage that reinforced its centrality. Because all four markets cleared through the same node, the Rothschilds possessed a real-time view of global capital flows that no government, no central bank, and no competitor could match [2]. Their private courier network delivered intelligence faster than official government channels [8]. This wasn't insider trading in the modern legal sense — it was the natural information asymmetry that accrues to whoever sits at the intersection of the world's major financial flows.

Modern parallel: the liquidity aggregation thesis

DeFi's hub problem

DeFi today looks remarkably like pre-Rothschild European finance: fragmented markets with limited interoperability, each operating under different rules, with no central node that connects them all efficiently.

A trader wanting exposure across DeFi's major asset classes — stablecoins, liquid staking tokens, governance tokens, real-world assets — must navigate dozens of DEXs across multiple chains, each with different pool structures, fee models, and liquidity depths. There is no single hub where gold-equivalent assets (BTC, stETH), bond-equivalent assets (tokenized treasuries, yield-bearing stablecoins), commodity-equivalent assets (tokenized commodities), and currency-equivalent assets (stablecoins across multiple chains) all converge through a unified settlement layer.

DEX aggregators like 1inch, CowSwap, and Paraswap are the early proto-hubs — they route across fragmented liquidity to find optimal execution, absorbing complexity so the trader doesn't need direct relationships with every pool. But they operate primarily within single chains. Cross-chain aggregation through protocols like Li.Fi and Socket is emerging but remains fragmented, meaning the hub function is incomplete. The trader who needs to move from stETH on Ethereum to USDC on Base to a tokenized treasury on Arbitrum is still navigating three separate settlement environments — the 19th-century equivalent of engaging separate brokers in London, Paris, and Vienna rather than routing everything through Rothschild.

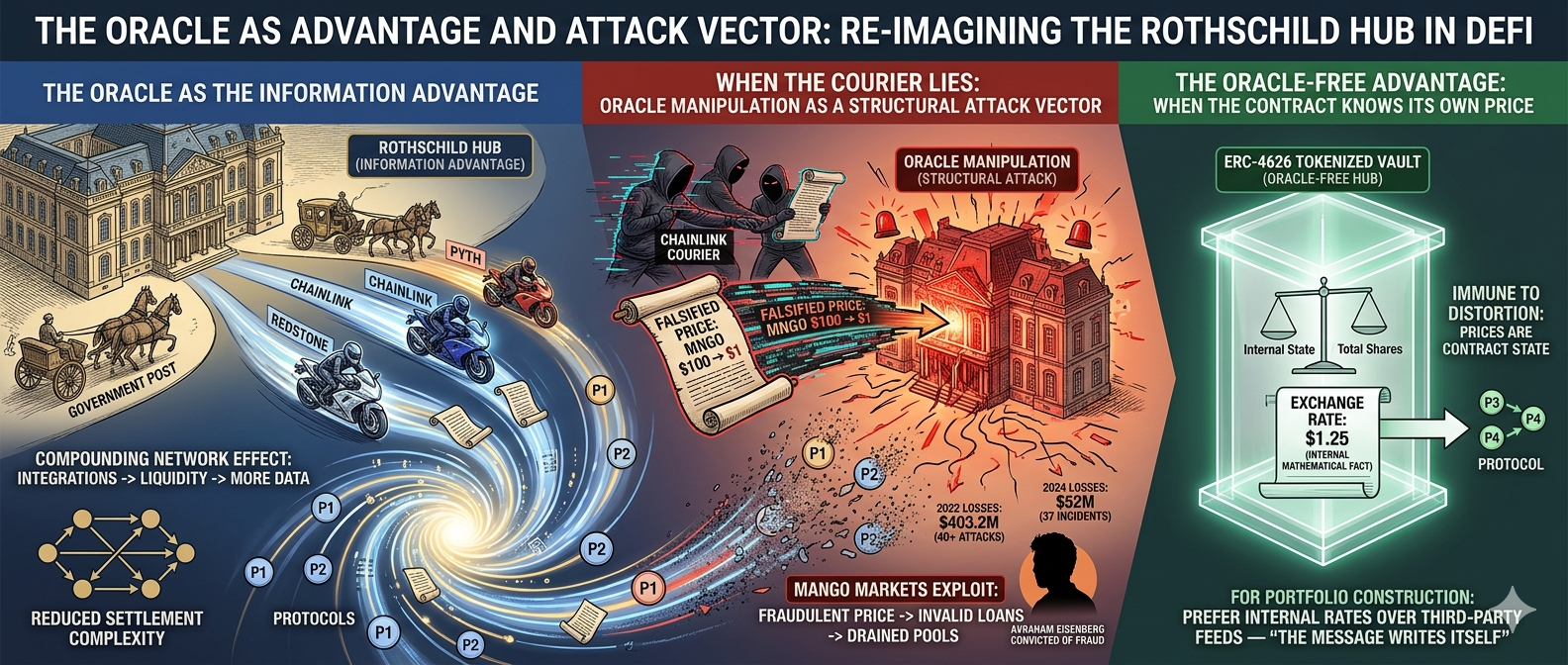

The oracle as the information advantage

The Rothschilds' courier network — which delivered market intelligence faster than governments — finds its modern parallel in oracle networks. Chainlink, Pyth, and Redstone are the courier systems of DeFi: they deliver price information across fragmented markets, enabling protocols to operate with a shared view of asset values. Just as the Rothschild hub's information advantage reinforced its centrality as a settlement node, oracle networks that provide faster, more reliable price feeds attract more protocol integrations, which attracts more liquidity, which generates more data — a compounding network effect.

The portfolio implication is direct: protocols that combine aggregation, cross-chain settlement, and oracle infrastructure are building the Rothschild hub of DeFi — the nexus node where multiple asset classes converge through a single trusted interface. These are not the protocols offering the highest yields. They are the protocols that reduce settlement complexity for everyone else.

When the courier lies: oracle manipulation as a structural attack vector

The Rothschild courier network was powerful because it was trusted. If a courier had been intercepted and the message altered, say a bond price falsified, a gold shipment misreported, the entire hub's decision-making would have been corrupted. The family guarded against this obsessively: couriers traveled in pairs, used coded correspondence, and operated dedicated routes separate from public mail [8]. The information advantage was only valuable because the information was accurate.

In DeFi, oracle manipulation is the modern equivalent. In 2022, protocols lost $403.2 million across over 40 attacks [18]; in 2024, it caused $52 million in losses over 37 incidents [19]. Attackers distort trusted price data, exploiting automated responses via flash loans to liquidate positions, issue invalid loans, or drain pools [20]. The Mango Markets exploit in October 2022 showed this: Avraham Eisenberg inflated MNGO's oracle price on thin markets, borrowed against it, and drained assets [21]. Convicted of fraud, it set precedent that this is manipulation, not clever trading [21]. Protocols depending on external prices carry inherent risk no audit fully eliminates; OWASP ranks it second in 2025 vulnerabilities [22].

The oracle-free advantage: when the contract knows its own price

This breaks the Rothschild analogy productively: what if prices didn't need transmission? ERC-4626 tokenized vaults achieve this. A yield-bearing vault token needs no oracle; convertToAssets returns its exchange rate on-chain from internal accounting [23]. Balancer V3 reads this directly via Rate Provider—no external feed to manipulate. This eliminates a key attack surface: prices are mathematical facts from contract state, immune to distortion. For the four-layer framework, Layer 4 hubs using oracle-free assets are safer, with fewer failure modes. In portfolio construction, prefer tokens reporting their own rates over those needing third-party feeds—the message writes itself.

Portfolio lessons: the four-layer framework complete

The complete liquidity risk assessment

The four-part mini-series now provides a complete framework for evaluating any DeFi position:

Layer 1 — Pool depth (Part 1): Is there enough market depth to absorb your exit? Are there multiple venues, or does all liquidity concentrate on a single DEX?

Layer 2 — Backstop (Part 2): Is there a lender of last resort when confidence breaks? The Eurodollar system had the Fed swap lines. What does your stablecoin have?

Layer 3 — Pipes (Part 3): Can you move the asset to where depth exists? Are bridges and settlement channels operational, audited, and battle-tested? The New York Clearing House operated through ten panics without interruption. Can your bridge say the same?

Layer 4 — Hub (Part 4): Is there a nexus node that connects your asset's market to other markets efficiently? Can you convert between asset classes — from yield-bearing stablecoins to governance tokens to liquid staking derivatives — without navigating five separate settlement environments?

Most DeFi participants evaluate only Layer 1. Sophisticated participants consider Layers 2 and 3. The Rothschild lesson adds Layer 4: the assets that retain value in a crisis are those connected to a hub that provides efficient conversion across multiple markets. Gold was valuable in the 19th century partly because of its intrinsic properties — but mostly because Rothschild made it instantly convertible into bonds, currency, and credit through a single interface. An asset that cannot be efficiently converted into other asset classes through a trusted hub is, in a crisis, only as liquid as its single deepest pool.

The hub premium

The Rothschild fortune was not built by creating assets. It was built by connecting them. The family sat at the intersection and charged for the complexity reduction. In DeFi, the protocols that will compound value over decades are those that position themselves as hubs — connecting fragmented liquidity into unified settlement, providing cross-market conversion, and accumulating the information advantage that comes from sitting at the center of global capital flows. The protocols building this layer are not glamorous. They are building the plumbing under the plumbing. And like the Rothschild house, they will outlast everything flowing through them.

Sources and references

[1] "Rothschild Family." Wikipedia. Five-branch network establishment and overview. https://en.wikipedia.org/wiki/Rothschild_family

[2] "The House of Rothschild — Investment Compass, Ep. 12." Kroker Equity Research (Substack), September 2025. Coordinated multinational operations, information networks. https://krokerequityresearch.substack.com/p/127-the-house-of-rothschild-investment

[3] "Rothschilds." Encyclopedia.com. Bond market dominance, multinational arbitrage, merchant banking. https://www.encyclopedia.com/history/encyclopedias-almanacs-transcripts-and-maps/rothschilds

[4] The Rothschild Archive. "The London Banking House: Rothschild and Gold." Official archive. https://www.rothschildarchive.org/business/n_m_rothschild_and_sons_london/rothschild_and_gold

[5] "N M Rothschild & Sons and the Royal Mint Refinery, London." GLIAS Journal, no. 15. Royal Mint Refinery lease and gold refining operations. http://www.glias.org.uk/journals/15-a.html

[6] "Rothschild & Co." Wikipedia. London Gold Fixing 1919–2004, gold price benchmark. https://en.wikipedia.org/wiki/Rothschild_%26_Co

[7] The Rothschild Archive. "Rothschild Timeline — Exhibitions." Brazilian independence loan, baronial grants. https://www.rothschildarchive.org/exhibitions/timeline/

[8] "Nathan Mayer Rothschild." Wikipedia. Courier network, intelligence advantage, Napoleonic War financing. https://en.wikipedia.org/wiki/Nathan_Mayer_Rothschild

[9] "Rothschild Family." Britannica Money. Five-branch establishment, government financing, industrial revolution. https://www.britannica.com/money/Rothschild-family

[10] "Origins of the London Bullion Market." London Bullion Market Association (LBMA). https://www.lbma.org.uk/market-standards/origins-of-the-london-bullion-market

[11] "Rothschild Banking Family of England." Wikipedia. Bank of England 1825 liquidity crisis, sovereign lending. https://en.wikipedia.org/wiki/Rothschild_banking_family_of_England

[12] The Rothschild Archive. "The London House History: N M Rothschild & Sons, 1836–1879." Royal Mint Refinery, commodity interests, railway finance. https://guide-to-the-archive.rothschildarchive.org/the-london-banking-house/depts/the-london-house-history/n-m-rothschild-sons-1836-1879

[13] "The Rothschild Family." EBSCO Research Starters. Multinational coordination, bond issuance, Continental operations. https://www.ebsco.com/research-starters/biography/rothschild-family

[14] Arnold, Anthony John. "Business Returns from Gold Price Fixing and Bullion Trading on the Interwar London Market." Business History, vol. 58, no. 2 (2016): 283–308. Rothschild role in gold fixing mechanism.

[15] Ferguson, Niall. The House of Rothschild: Money's Prophets, 1798–1848. Penguin Books, 1998. Definitive scholarly history of the Rothschild financial network.

[16] Cassis, Youssef. Capitals of Capital: The Rise and Fall of International Financial Centres, 1780–2009. Cambridge University Press, 2006. London's structural advantages as a financial hub.

[17] Flandreau, Marc and Juan H. Flores. "Bonds and Brands: Foundations of Sovereign Debt Markets, 1820–1830." Journal of Economic History, vol. 69, no. 3 (2009): 646–684. Rothschild role in sovereign bond market formation.

[18] Cyfrin. "The Full Guide to Price Oracle Manipulation Attacks." 2024. https://www.cyfrin.io/blog/price-oracle-manipulation-attacks-with-examples

[19] Three Sigma. "2024 Most Exploited DeFi Vulnerabilities." 2025. https://threesigma.xyz/blog/exploit/2024-defi-exploits-top-vulnerabilities

[20] CertiK. "Oracle Wars: The Rise of Price Manipulation Attacks." May 2025. https://www.certik.com/resources/blog/oracle-wars-the-rise-of-price-manipulation-attacks

[21] Chainalysis. "Oracle Manipulation Attacks Rising: A Unique Concern for DeFi." August 2023. https://www.chainalysis.com/blog/oracle-manipulation-attacks-rising/

[22] OWASP. "SC02:2025 — Price Oracle Manipulation." Smart Contract Top 10. https://owasp.org/www-project-smart-contract-top-10/2025/en/src/SC02-price-oracle-manipulation.html

[23] EIP-4626: Tokenized Vault Standard. Ethereum Improvement Proposals. https://eips.ethereum.org/EIPS/eip-4626

Legal disclaimers and disclosures

Educational purpose only: This content is provided exclusively for educational and historical research purposes. It should not be construed as investment advice, financial planning guidance, policy recommendations, or official economic analysis. Any contemporary parallels or policy discussions are presented as academic analysis, not recommendations for action. Historical patterns provide context for learning but do not predict future financial system outcomes or investment performance.

AI-assisted research disclosure: This historical analysis was researched and written with substantial assistance from artificial intelligence technology (Claude, Anthropic). While extensive efforts were made to verify all statistical claims, citations, and institutional analysis against authoritative sources, readers should independently verify any information before relying on it for academic, professional, investment, or policy purposes.

Accuracy and liability limitations: While extensive effort has been made to ensure historical accuracy through authoritative sources, the authors make no warranties about completeness, accuracy, or currency of information. Historical interpretation involves scholarly judgment and academic debate. Economic data may contain revisions, measurement inconsistencies, or reporting variations across different time periods and institutional sources.

Liability protections: The authors, publishers, and Sagix Apothecary assume no responsibility for errors, omissions, or consequences arising from the use of this information. This includes any errors that may result from AI assistance in research, writing, or data analysis. Users assume full responsibility for any decisions or actions taken based on this content.

Investment risk warning: Historical financial analysis does not constitute investment advice or recommendations. Past performance, whether historical or hypothetical, does not guarantee future results. All investments carry risk of loss, and readers should conduct their own research and consult qualified financial advisors before making investment decisions.

No professional relationship: This content does not create any professional, advisory, fiduciary, or client relationship between the reader and Sagix Apothecary, its authors, or affiliated entities. Readers seeking financial, investment, legal, regulatory, or policy guidance should consult qualified professionals licensed in their jurisdiction.

Methodological note: This analysis synthesizes findings from official Rothschild Archive publications, peer-reviewed academic journals, authoritative historical encyclopedias, and institutional records from the London Bullion Market Association. The numbered citation system allows readers to verify specific claims against original sources rather than relying on secondary interpretations. All quantitative data and statistical analyses are drawn from the referenced academic literature rather than independent calculation.

Contemporary financial systems: References to modern financial systems, cryptocurrency protocols, or DeFi mechanisms are made for educational comparison purposes only. These comparisons do not constitute endorsements, recommendations, or predictions about the performance or suitability of any current financial products or services.

Publication information: Last Updated: March 2026 | Series: The Druid Deep Dive | Publisher: The Genesis Address LLC